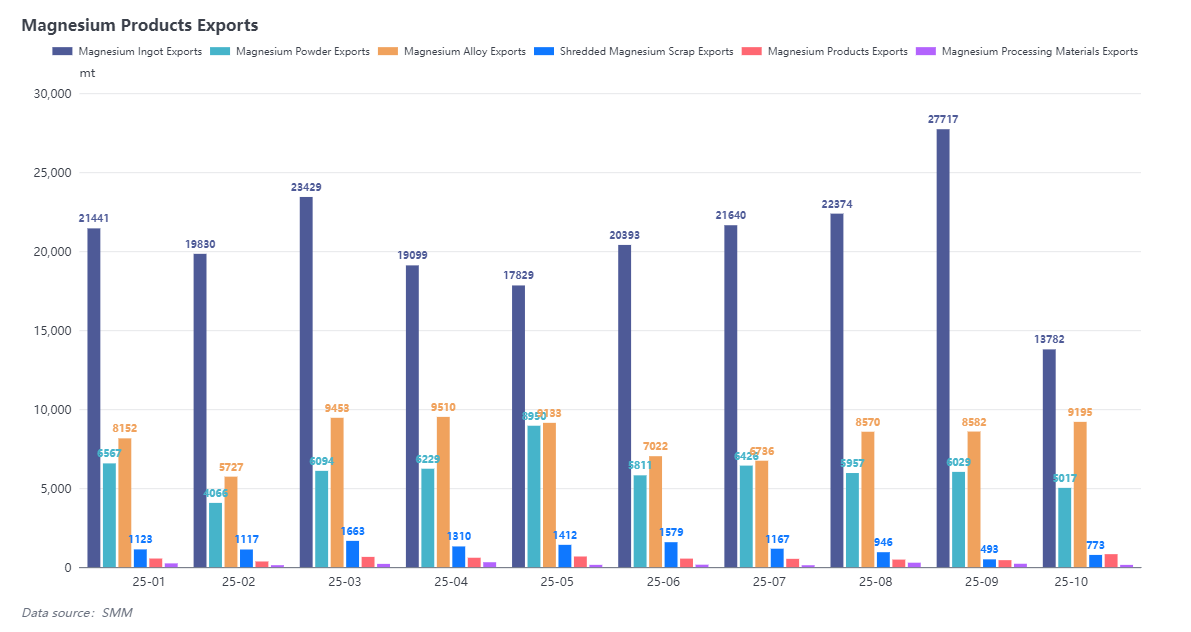

October Magnesium Product Exports Severely Contract, Total Volume Down 31.6% MoM

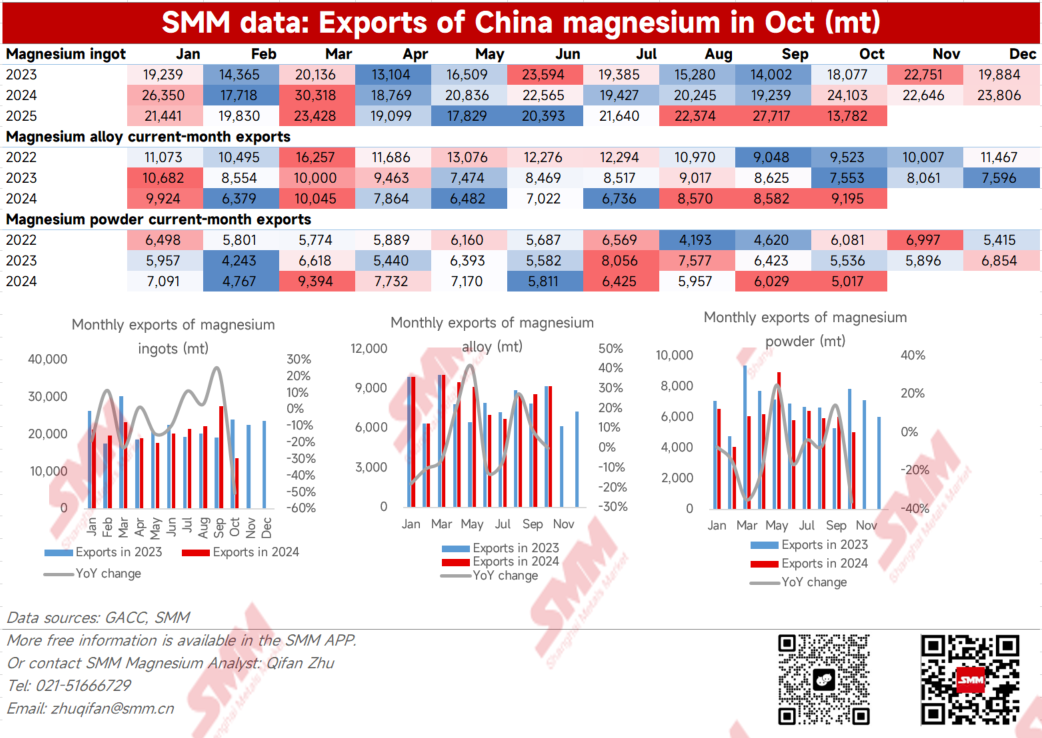

In October 2025, China's total export volume of magnesium products was 29,700 tonnes, a decrease of 31.6% month-on-month. The cumulative export volume for 2025 reached 370,000 tonnes, a cumulative year-on-year decrease of 3.55%. The export decrease this month primarily stemmed from magnesium ingot products. Although they remain the main category in magnesium product exports, the export volume this month was only 13,800 tonnes, a significant reduction of 50% MoM, also hitting the lowest level since the beginning of this year, forming a sharp contrast with the historical high of the previous month, indicating a notable contraction in export scale.

According to SMM research, the contraction in October exports was mainly affected by two major factors: Firstly, the National Day holiday in early October; the eight-day holiday caused market trading activities to temporarily slow down, with basically no new order inquiries during this period. It also prompted the shipment schedules for some port orders to be brought forward or delayed, further exacerbating inventory pressure on the factory side. Secondly, news regarding export customs declaration controls in October had been circulating in the market since August. Most export traders and downstream end customers, concerned about potential impacts on Q4 order shipments and prices, chose to lock in order prices in advance at the end of August and September, and concentrated shipments ahead of the end of September. Therefore, the higher export volume in September already included some orders originally scheduled for October, and even November-December, consequently leading to a significant decline in October export data. Affected by this, export volumes from early October to mid-October remained consistently low. It was not until the customs declaration process returned to normal in late October that new overseas orders were gradually placed, and port shipments gradually recovered.

Significant Divergence in Magnesium Market Exports; Magnesium Alloy Becomes October Highlight

Looking at specific products, magnesium ingot exports in October totaled 13,800 tonnes, down 50.28% MoM and 42.82% year-on-year; the cumulative export volume for 2025 was 207,500 tonnes. As the key category supporting overall export performance, the sharp decline in magnesium ingot exports reflects significantly weak downstream demand in October. This is partly attributed to the aforementioned advance pulling of export orders, and also reflects the less optimistic performance of the mainstream downstream markets - the aluminum industry and automotive market - in the second half of the year. The weak export trend further intensified the downward pressure on domestic magnesium ingot export prices.

Magnesium powder exports in October totaled 5,017 tonnes, down 16.79% MoM; the cumulative export volume for 2025 was 61,000 tonnes, a decrease of 12.11% year-on-year. Since the beginning of this year, the magnesium powder export market has continued to perform weakly overall, with transactions mostly driven by rigid demand. Entering the second half of the year, downstream orders substantially decreased, especially affected by reduced demand in areas like desulfurizing agents. Overall exports are basically supported by rigid demand, with overseas orders showing a continuous contraction trend.

Magnesium alloy exports in October were 9,195 tonnes, an increase of 7.14% MoM; the cumulative export volume for 2025 was 82,000 tonnes, a slight increase of 0.3% year-on-year. Since August, magnesium alloy export volumes have continued to maintain growth, reflecting a significant increase in overseas orders for magnesium alloy. However, looking at the full year dimension, the overall export scale is basically flat compared to last year, indicating that the growth in Q3 was primarily used to compensate for the order trough in Q2. Overall, the overseas market demand for magnesium alloy throughout the year has been generally stable, similar to last year's level. Potential future demand growth is expected to mainly come from the continuous advancement of die-casting technology, promoting the further expansion of magnesium alloy applications.

Steady Recovery in European Demand; China's Magnesium Exports Focus on Three Major Markets

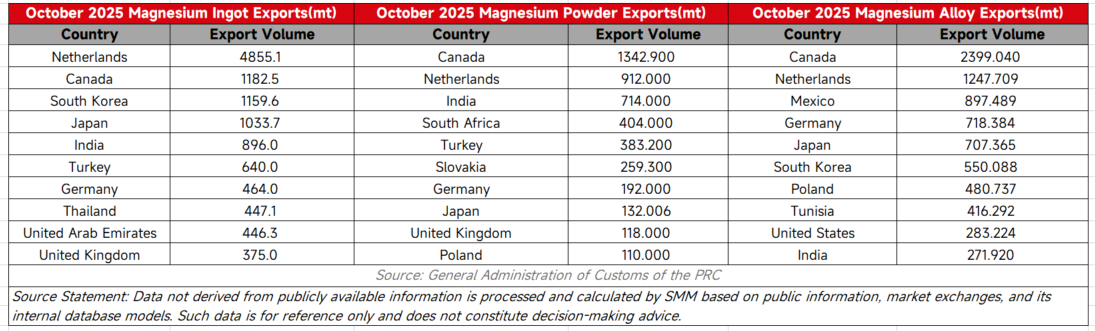

Looking at the main export destination countries in October, the Netherlands remains the core export market for magnesium ingots, with monthly exports reaching 4,855 tonnes, reflecting the relative rigidity and stability of demand in Europe. Canada is an important export country for magnesium powder and magnesium alloy, with exports of magnesium powder to Canada at 1,342 tonnes and magnesium alloy to Canada at 2,399 tonnes.

From the perspective of export market distribution, Chinese traders are currently mainly focusing on incremental opportunities in regions like Europe and Canada. European order patterns are usually more regular, and from the demand trend perspective, its market is showing a gradual recovery trend in the second half of the year. Japanese and South Korean orders better reflect immediate demand, with delivery cycles generally controlled within one month. Canada has become an important distribution hub for North American trade and may serve as a key transit point to the US market.

Short-term Exports Unlikely to Shake Off Weakness; Forward Order Pull-forward Intensifies Volatility

Looking ahead, exports in November are expected to remain relatively weak. However, as some quarterly orders for rigid demand enter the delivery phase, the overall export scale may slightly recover compared to October. Nevertheless, due to the significant pulling forward of future orders in September, the total export volume for the entire fourth quarter of this year is expected to remain at a low level.

From a price trend perspective, current prices have fallen to the lower range of the market. Some overseas customers, based on market considerations, might choose to lock in orders early. According to SMM research, many orders for Q1 2026, or even the first half of 2026, have entered a watchful or early release phase in November. These orders might again pull forward some future demand, potentially leading to a new round of fluctuations and volatility in export volumes.